The goal was to create a model to get events which then a Random Forest Classifier can then be fit on certain statistical properties to see an improved accuracy.

The pattern to find in Foregin Exchange data was called the Tripple Barrier Method.

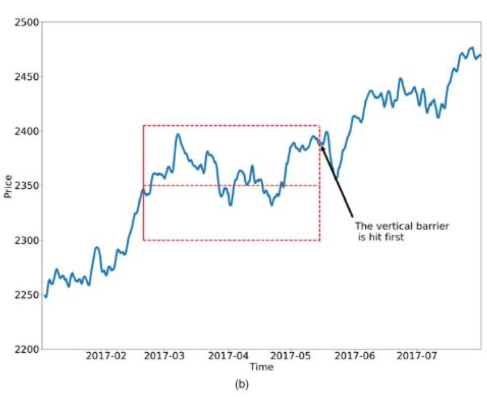

Table 1: As seen, if a certain section of the market touches the top barrier first then that means that is a positive occurrence of the class if it meets the vertical barrier or bottom barrier then it is a negative class.

Table 1: As seen, if a certain section of the market touches the top barrier first then that means that is a positive occurrence of the class if it meets the vertical barrier or bottom barrier then it is a negative class.

Once the events are chosen then statistical properties are gathered about the event dates and a Random Forest Classifier is then fitted on the event data.

The Github: Link

The online version can be found here: Link